How is the Super App of Large Commercial Banks 'Assembled'?

In recent years, driven by the rise of Internet finance platforms and banks' mobile digital transformation, banking transactions have been steadily moving from offline to online. More users now prefer using mobile banking apps for payments, transfers, and financial management, underlining the growing significance of these applications.

iResearch's 2022 analysis of China's mobile banking apps reveals that the average rate of non-counter transactions in the banking sector has been increasing since 2016, exceeding 90% in 2021. By June 2022, the monthly active total of mobile banking apps in China reached 570 million, marking a notable expansion of the user base. However, concurrently, the number of physical bank branches has been decreasing annually. For instance, the six major state-owned banks in China saw a reduction of over 3,000 branches from 2016 to 2021.

As online transactions grow, mobile banking apps are encountering significant challenges, especially in managing large user bases efficiently.

Efficiently Operating a Vast User Base

Mobile banking apps are key for banks to serve their customers, but they face issues in feature richness, user operations, and agile development, impacting customer satisfaction and loyalty.

1、Challenges in IT Architecture for Agile Delivery: Mobile banking apps need frequent updates for various online marketing scenarios. However, the complexity and increasing integration time of outdated system architecture codes make iterative releases costly. The tightly coupled systems hinder efficient agile iterations.

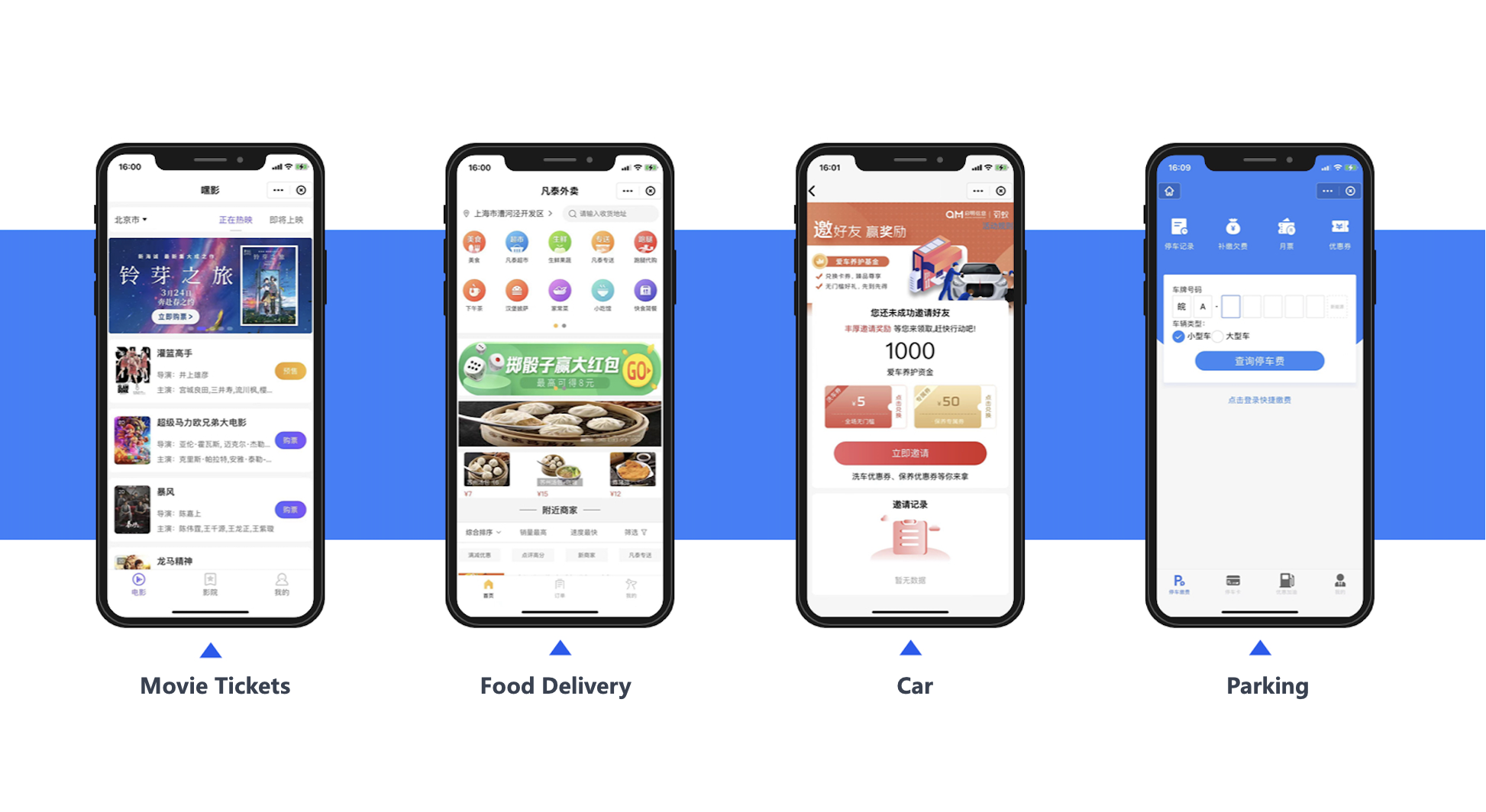

2、Limited Consumer Scenarios: Many mobile banking apps offer only basic financial services like transfers, inquiries, and payments. Integrating these services with daily life and consumer scenarios remains a challenge, resulting in a lack of services meeting diverse user needs.

3、Low User Engagement: Most internet traffic is concentrated on platforms like WeChat, Alipay, and TikTok. Banks have been expanding services through mini-programs on platforms like WeChat to attract users. However, this has further reduced the engagement of mobile banking apps.

In the digital transformation era, addressing these common issues in banking apps is crucial.

Mini-Programs in Marketing and Operations Strategy

With mobile usage rising, platforms like WeChat capture significant user traffic. Banks have been deploying business services through mini-programs to adapt to user habits. Major banks like ICBC, China Construction Bank, China Merchants Bank, and Agricultural Bank of China have mini-program user numbers exceeding 100 million. ICBC's "ICBC Life" mini-program alone has 120 million monthly active users. The types of mini-programs launched include:

- Financial Services: Providing account inquiries, transfers, and payments.

- Marketing and Promotions: Offering coupons, discounts, and personalized recommendations.

- Consumer Finance: Including installment payments and loans.

- Investment and Financial Management: Services like funds and stocks.

Advantages of Mini-Programs

Mini-programs are lightweight and don’t require installation. They offer a high-quality user experience similar to native apps and spread quickly, suitable for major social platforms. Technically, mini-programs support rapid development and deployment, addressing the lengthy release process of mobile banking apps.

A Major Commercial Bank’s Strategy

A major commercial bank is creating a super app based on its mobile banking app, using mini-programs to quickly assemble internal and external services. This decouples app functions, managing business mini-programs through backend operations.

Background of the Mobile Banking App

- User Base: Over a hundred million.

- Key Strategies: Upgrade technological architecture, develop a super app ecosystem, and multi-channel operations.

The bank chose FinClip mini-program container technology, ensuring data privacy and security. FinClip's SDKs and management tools enable the bank to control its technological ecosystem.

Developing with FinClip

By integrating the FinClip SDK, the bank's app can run various business functions as mini-programs. This supports agile development and hot updates, minimally interfering with the app. Mini-programs balance performance and flexibility, providing an interactive experience close to native applications. With FinClip, the app supports third-party functions, addressing expansion challenges.

Creating an Open Banking Super App

Using FinClip, the bank introduced numerous high-quality service mini-programs, combining them with its financial services. This approach creates an open banking ecosystem, similar to operating an app store.

Multi-Channel Operations and Enhanced User Engagement

The bank synchronized its WeChat mini-programs to its app using FinClip, guiding users to its mobile platform. This approach enhances app engagement, offering a service experience akin to WeChat's mini-programs.